Blockchain is on everyone’s lips these days – nowhere more so than in the trade finance world. This technology has the potential to clamp down on fraud, streamline supply chains, and enhance companies’ liquidity. As the prime facilitators of trade, banks are as eager as any to bring the benefits to their corporate clients.

Making blockchain a reality, however, will take time and require a practical approach. Banks will have to identify targeted “use cases” – determining exactly how and where blockchain can bring improvements.

Strong collaboration between financial institutions and technology firms will be needed to bridge technical gaps, while success will depend on agreeing common standards and frameworks.

Back to basics: how blockchain works

Blockchain technology relies on a “distributed ledger” – a cache of digital information to which all users of a certain computer network have shared access.

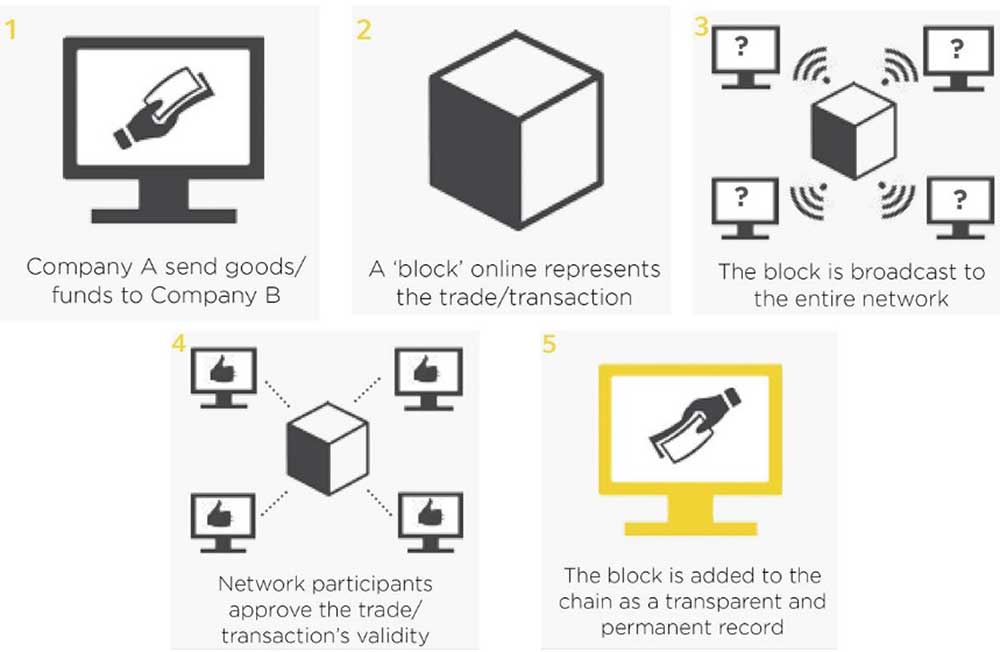

As stages 1 & 2 of the diagram show, any addition to this record – created by a new trade or transaction – is logged as a “block” of data. All members of the network are notified of this action (stage 3), and at least one of the members must accept the change as valid (stage 4). Once verified, this new block is “chained” to the previous blocks of data (stage 5).

Bulking up security in trade

This authenticated data chain results in high degrees of transparency and security most welcome in the trade industry. The ledger is visible and accessible (i.e. “distributed”) to all counterparties involved in trade – whether banks, buyers, sellers, shipping companies, insurers, forwarders, customs officers, inspection bureaus or regulators. Should a new transaction be attempted, this entire network must first accept any modification to the chain as legitimate.

Blockchain could thus form a key ally for banks in their fight against fraud. Banks must always be on the lookout for the risk of “double-financing”, for example – the chance that another bank has already been allocated the trade’s receivable, or that another transaction is already using the invoice presented for financing as collateral. The permanent and essentially tamper-proof record offered by blockchain would mitigate this threat.

Blockchain facilitates automation and risk mitigation

Yet the advantages do not stop there.

The distributed ledger would offer a bank comprehensive and real-time insights into its corporate customer’s entire supply chain – from the initial order of purchase, to assembly, inventory, payment and final delivery.

Without having to spend time and resources on manually processing and matching data, the bank could more efficiently identify positions in the supply chain where risk mitigation and financing are needed. Funds could be released in a timelier manner, and the risk of non-payment would be eliminated, enhancing with the company’s liquidity as a result.

“Smart contracts” represent another exciting prospect of blockchain. These contracts are designed to carry out pre-defined actions automatically when set off by a particular event in the supply chain. For example, once the delivery of goods to an importer has been effected, a smart contract would ensure that funds are automatically released to the exporter.

At Commerzbank, we’ve already used the underlying concept of the smart contract when facilitating trade with the Bank Payment Obligation (BPO). The BPO is a new trade finance instrument positioned between open account and the letter of credit. It provides payment assurance on the automatic exchange and matching of digital trade data – without presentation of paper documents – to complete a transaction.

The journey to blockchain is far from straightforward

The application of the smart contract idea is certainly an important step towards realising the full potential of blockchain in trade. But a range of challenges will be met along the way.

For a start, banks must establish exactly how distributed ledgers can enhance their corporate customers’ trade. Whether they want to speed up provision of financing, improve a customer’s working capital, or mitigate payment risk, banks will need to identify the right use cases for blockchain, and find exactly where new solutions are needed. This will be much more productive than merely attempting to replace tried-and-tested trade solutions, such as the letter of credit or guarantee, with an alternative based on the distributed ledger.

There will also be technical challenges to overcome. Banks and companies will need to invest resources into developing blockchain’s digital interfaces, spend time getting to grips with the technology, and ensure that data security in their blockchain systems is up to scratch. They will also have to agree to standards that can ensure that the software underpinning new blockchain processes will work with legacy systems.

Meanwhile, the trade finance industry will require crucial harmonisation when it comes to offering and using blockchain platforms.

The standout advantage of blockchain is its interconnectivity. This would be wasted if different trade finance parties used various distributed ledger technologies, underpinned by incompatible systems.

Collaboration will be the key to integration

Progress, therefore, will rely on the banks, technology providers and all other stakeholders in the complex trade finance ecosystem being able to work together. They must not only agree to set standards, but also to share insights and useful experiences.

It is for this reason that the R3 consortium, a group of more than 70 financial institutions including Commerzbank, are committed to the research and development of distributed ledger technology. The Euro Banking Authority Working Group for Cryptotechnology for Trade Finance is another group which seeks to explore use cases for blockchain for corporate customers.

Blockchain has the true potential to enrich companies’ trade – but success will take time, collaboration, and hard work from the banks.

disqus comments