When you hear about export credit insurance, it may not come to mind as an option for your small business. Actually, trade credit insurance can make sense and be accessible for businesses of almost any size, even microbusiness exporters. One insurance company explains that “a modest company may earn most of its revenues from a single customer. The owners will want an insurance policy to protect their bottom line in the event that customer defaults on their payments, dissolves their own business, or files for bankruptcy.”

To address this issue, export credit agencies (ECAs) provide export financing, as well as various types of risk insurance or guarantees. This insurance protects exporters against non-payment of receivables by foreign importers.

Key factors to be considered when purchasing export credit insurance include:

- The risks covered by the insurer (political, commercial)

- The extent to which risks are shared between the insurer and the insured party (also known as the co-insurance ratio)

- The services provided by the insurer, including credit reports and their analysis, country risk information and information with respect to the insurer’s own experience in the country or region

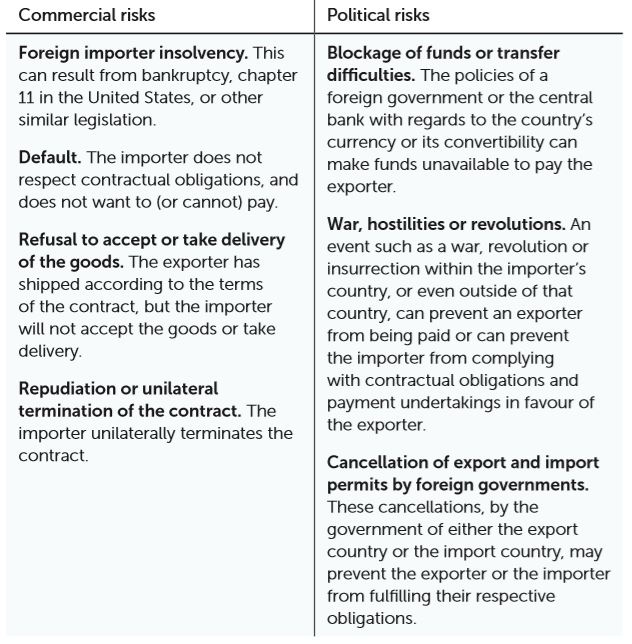

Export credit insurance usually covers two main categories of risk that concern exporters the most—commercial and political risk.

Insurance policies normally cover commercial and political risks

Export credit insurance does not cover losses from commercial disputes between exporters and foreign importers. Usually, these disputes must be resolved to the satisfaction of the insurer before claims are considered for payment. For example, if a foreign customer refuses to pay for goods on the grounds that the shipment was not what was ordered, the claim may have to be adjudicated by a court of arbitration in favour of the exporter before the latter could collect on the insurance policy.

Want to learn more about how to minimize your organization’s exposure to financial risk using tools such as credit insurance, guarantees and bonds? Check out the FITTskills International Trade Finance online course.

Export Credit Insurance—Risks and Premiums

Export credit insurance premiums are directly tied to the risk of a transaction and the extent to which the exporter is willing to bear some of that risk. Insurers usually require some risk sharing on the part of the exporter to ensure the exporter acts in the best interest of both the company and the export credit agency.

One method of risk sharing is adding a co-insurance ratio. In a 90 percent coinsurance policy, the insurer, for example, pays 90 percent of total claim while the exporter absorbs the remaining 10 percent loss. Risk sharing in this manner tends to ensure that exporters remain mindful of risk issues, and work to mitigate or optimize risks in a given transaction. Having a stake in the transaction avoids, or reduces, the chances of exporters pursuing highly speculative business without regard for potential loss.

Deductibles are another method of risk sharing. A deductible requires the exporter to take the first loss from an uncollected export receivable, up to a specified amount.

For example, if a Brazilian exporter has a BRL 10,000 deductible policy, the exporter would absorb the first BRL 10,000 of a BRL 50,000 loss. The insurer would indemnify the insured based on the eligible loss of BRL 40,000 to which the policy co-insurance ratio would be applied. In this case, the insurer would make a claim payment of BRL 36,000 if the co-insurance ratio was 90 percent.

Deductibles generally serve to reduce the administrative costs the insurer would incur from processing very small claims.

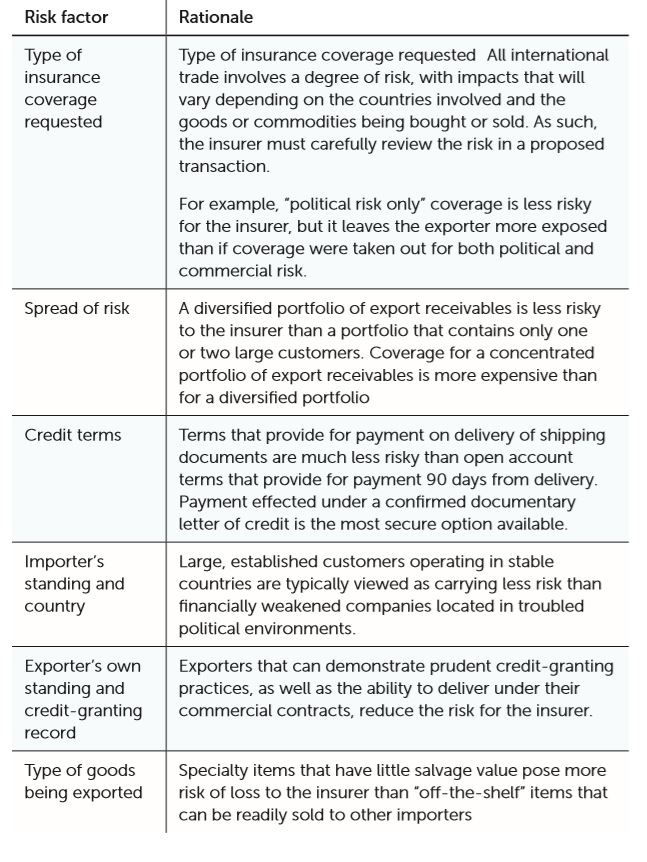

The insurer determines the risks involved in a transaction by reviewing a number of key factors:

If the exporter acts to reduce the level of risk to the insurer by improving on those key factors, lower insurance premiums will be charged. In most insurance policies, insurers require the insured to obtain the necessary coverage prior to shipment. In this situation, the insured may request a particular limit that helps them cover the total amount of shipment for one transaction or may request a global amount that can help cover all future shipments. Insurance premiums are payable directly to the ECA based on the policy conditions, either on the limit requested or on the amount of the global limit used.

Case Study: Going Global with an Export Credit Agency

Over the course of 30 years, MarineNav Inc. (MNI) has built an international reputation for its work in integrated marine traffic control systems. Based in Los Angeles, California, MNI provides highly technical solutions to clients in the United States and Canada, as well as countries including Tanzania, Libya, Algeria, Morocco, Democratic Republic of Congo, Venezuela and Colombia.

Many of the markets that MNI trades in have challenging political environments, causing contract and construction delays, deferred billing of completed work and collection of receivables. These delays have a significant impact on MNI operations, including obstructing progress of other contracts.

To overcome these challenges, MNI benefitted from a variety of services offered by its ECA, including:

- Performance letters of guarantee: MNI contracts require the company to issue performance letters of guarantee to secure the buyers. This 100 percent ECA guarantee enabled MNI to issue the required guarantees when the contracts were signed.

- Political risk insurance: During the Arab Spring in Libya, MNI lost all of its assets in that country. The coverage provided through its political risk insurance allowed MNI to replace these assets right away.

- Working capital financing: MNI took on four contracts at once and were unable to secure adequate financing using the company’s line of credit. MNI received working capital financing provided by the ECA in partnership with MNI’s bank. This financing allowed MNI to complete the contracts and maintain its sterling international reputation.

- Direct lending: Some of MNI’s prospective clients struggle with access to financing within their countries. To resolve this challenge, the ECA will lend directly to foreign buyers or provide a guarantee to a foreign bank that would then lend the client the money needed to make the purchase.

The support of an ECA was instrumental to MNI’s success, providing market intelligence and financial support that allowed the company to grow by 200 percent on the international market.

disqus comments