Doing business in international markets is different from handling domestic business transactions on many levels.

A company that has decided to export its product or service to a new market or to buy from a new supplier in a different country cannot take for granted that the transactions will be viable, profitable or provide goods and/or services at a price and quality that are competitive. An exporter must ensure acceptable and timely returns on their financial investment in proportion to the associated costs and risks.

A transaction may prove unrealistic if the cost of entering a market is too high, the competition is too challenging or the price in the new market is not competitive. It is also not viable if the resulting sales generate losses or cannot adequately support the cost of doing business.

An importer needs to be sure that the product or service remains appealing even after factoring in the landing costs (all costs associated with the delivery of the goods and/or services to the country of destination), the packaging and the expense of any up-front travel and due diligence.

Exploring and entering new international markets is expensive, as costs can involve:

- Travel

- Communication

- Market research

- Packaging

- Insurance

- Professional services fees

- Banking charges

While the costs and risks of new trade ventures may be considerable they can be mastered with careful planning and preparation. With any new business venture, financials must remain a top priority.

Identifying cost and price elements

Conducting business internationally requires planning for foreign exchange rates, varying inflation rates and applicable laws and regulations—at home and abroad. Market factors to consider include competition, market share and the purchasing power of potential multinational clients.

Pricing a product for export is one of the most important steps in evaluating the viability of transactions and should be as accurate as possible. The cost of the sale will set the lower limit at which the export price will be set, and this will in turn set the basis for the negotiation between the exporter and importer.

2 approaches to product costing

-

The most frequently used – cost-plus approach

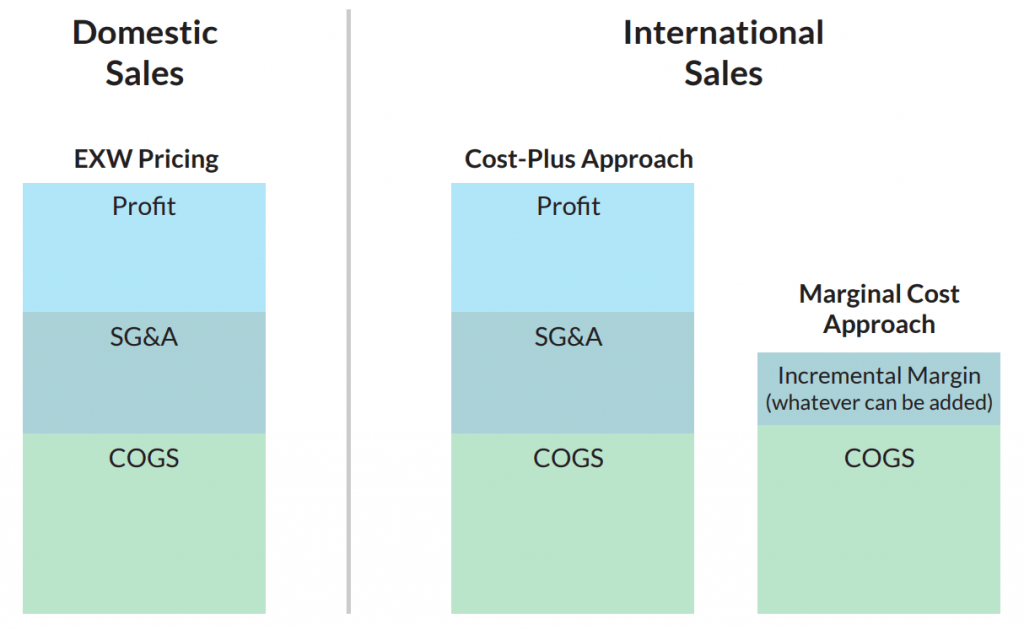

Cost-plus is a method where product costing is based on a calculation of the Cost of Goods Sold (COGS) and a calculation of Selling, General and Administrative (SG&A) expenses. These two broad categories of costs, COGS and SG&A, are used to determine the underlying product cost. On top of this, an additional profit margin is also expected. In exporting, additional costs must be recovered within the pricing structure that is used for export sales.

While cost-plus pricing is fairly straightforward, it does not work well in many export markets. For example, a cost-plus approach does not account for the incremental costs within the distribution channel. It also does not account for an understanding of market pricing, leading to the situation where a price could, in some circumstances, be too low. This can result in a deal with an importer or distributor that produces a disproportionate share of the profits.

Often, a cost-plus approach will result in a price that is too high. Export pricing tends to be market-driven, which means that pricing is generally dictated by market conditions.

The margin expectations of retailers and distributors are not particularly flexible, and supply chain costs (e.g. shipping costs, insurance, trucking) are similarly constrained. Consequently, many exporters are faced with a scenario where market-driven pricing is the starting point for calculations. From here, they must work backwards from the customer to ensure that suitable margins for the retailer and the distributor are available, and that all other supply chain/ distribution costs can be covered. This leaves the company in a position where normal Ex Works (EXW) pricing of their product is often not low enough, leading to potential deals falling through and additional market share remaining elusive.

EXW pricing stands for Ex Works which is an Incoterms® rule that specifies that, for the price being quoted, the exporter of goods is responsible to make the products readily available for pick-up at the company’s location for the importer. In other words, this price doesn’t include any additional costs associated with getting the product to the importer.

Want to learn more about how to ensure your business remains financially viable by analyzing the cost and pricing or your imports or exports? Check out the FITTskills Cost and Price Analysis online workshop!

2. Marginal-cost approach

Many exporters use a marginal-cost (or variable-cost) approach to export pricing. In this approach, a company that is already profitable in its own domestic market will make a strategic decision to carry the burden of all the company’s SG&A expenses or overheads on domestic sales. New/incremental overheads incurred specifically for export sales might be added as burden to the cost of exported goods, but, otherwise, the company uses only the COGS as the baseline product cost for export pricing.

This gives the exporter a much lower cost basis and the ability to be responsive to potential export sales, for example, where market-driven pricing and supply chain costs demand a very low EXW price for export.

There are also incremental costs for export which are largely inflexible and market-driven. Exporters receive proposals from importers that have been based on market pricing and must then work backwards to ensure that distributors and retailers can earn adequate margins that cover, for example, duties, shipping and insurance.

Consequently, the price target that the exporter needs to meet for EXW pricing is often too aggressive for the cost-plus approach and results in unfeasible deals. By contrast, those who use the marginal-cost method start with the COGS and add only the amount of incremental margin they can get away with to meet the target price.

In general, the use of a marginal-cost pricing approach for export markets will generate incremental sales that improve the overall profitability of the business. The additional sales volume will often result in better supplier pricing, and the incremental margins earned when the sale price is greater than the COGS will still contribute toward overall profits.

This is not always intuitive since many companies are used to seeing domestic “cost” breakdowns that include COGS, SG&A and profit. But marginal-cost pricing begins with COGS as the baseline cost, and it is therefore much more aggressive. This approach gives the export sales department a stronger position to make export deals.

Before applying a marginal-cost pricing approach, a company must already be profitable, and the domestic forecast should be conservative and achievable to ensure that SG&A is covered with margins earned on domestic sales.

Avoid “dumping”

Marginal-cost pricing can also be considered “dumping” by the importing country in some situations. Dumping occurs when the price of a product sold in the importing country is less than the price of that product in the market of the exporting country, and when competitors that are based in the importing country are injured.

Goods sold into the export markets at extremely low prices should be sufficiently different from the goods sold in the domestic market, for example with different packaging/labelling. This will minimize the risk that the exported goods will be shipped back to the exporter’s home market and sold back to the company’s existing customers via the gray market.

Which pricing strategy will work best for you?

Before adopting a certain pricing strategy, a company will need to carefully consider international pricing constraints in the form of local regulations or legislation, including anti-dumping legislation, resale price maintenance regulations, as well as price ceilings and price level reviews.

A pricing strategy, like other aspects of the financial plan, will be flexible and fine-tuned according to the dynamics of the global market.

The ultimate viability of a company’s international business strategy will depend on how well a product or commodity is priced to optimize profitability.

disqus comments